Stock Market Outlook entering the Week of June 15th = Uptrend

- ADX Directional Indicators: Uptrend

- Institutional Activity (Price & Volume): Uptrend

- On Balance Volume Indicator: Uptrend

ANALYSIS

The stock market outlook stays in an uptrend, despite intensifying conflict on the world stage.

The S&P500 ( $SPX ) lost 0.4% last week. The index sits ~6% above the 50-day moving average and ~3% above the 200-day moving average.

SPX Price & Volume Chart for June 15 2025

The ADX, Institutional Activity, and On-Balance Volume are all in bullish territory. Distribution days remain low, but are worth watching over the next week or two.

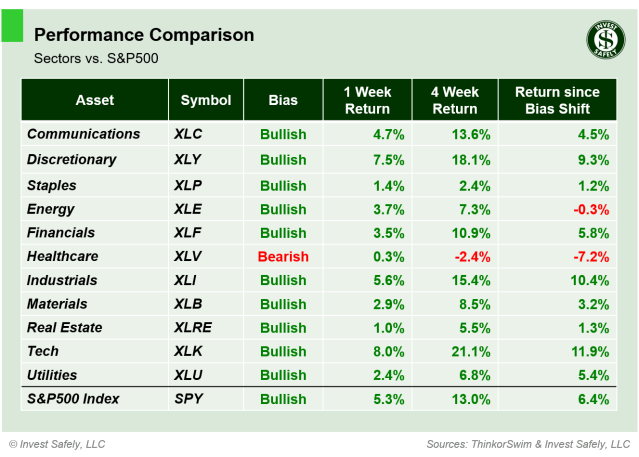

S&P Sector Performance from Week 24 of 2025

Energy ( $XLE ) led sectors higher last week, while Industrials ( $XLI ) lagged. Energy ( $XLE ) and Healthcare ( $XLV ) improved to bullish bias.

Sector Style Performance from Week 24 of 2025

High Beta ( $SPHB ) was the best performing style for the second week in a row, and Momentum ( $MTUM ) lagged. High Dividend ( $SPHD ) improved to bullish bias.

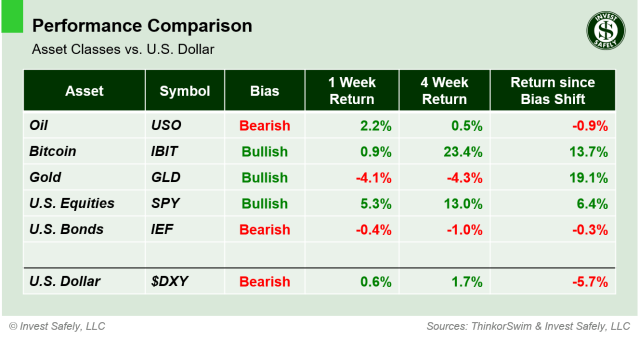

Asset Class Performance from Week 24 2025

Oil ( $USO ) led assets higher again last week, while the U.S. Dollar was the worst performer. U.S. Bonds ( $IEF ) improved to neutral again, continuing its recent oscillations between bias levels.

COMMENTARY

The uptrend in equities has remained quite resilient despite recent increases global conflict. Many market participants point out that the typical “flight to safety” trade (U.S. bonds) hasn’t occurred, so financial markets are saying all is well. That’s no reason to get complacent.

This time around, flows shifted more toward hard assets like gold or platinum, rather than U.S.-based assets like the dollar and bonds. Even silver has been on the move. So the flight to safety is on, just not into the traditional allocations.

The volatility index ( $VIX ) is back above 20 as well, signaling elevated risk and choppy price action ( <20 = low risk / calm, 20-30 = elevated risk / choppy, >30 = high risk / crash ).

For now, continue harvesting gains from outperforming / overbought areas and redeploy to those that are lagging / oversold, within assets showing bullish bias. But be aware that the investing environment can and does change quickly.

Inflation data rose slightly in May, though not as much as anticipated in most cases. Headline CPI rose 0.1%, while Core CPI remained steady.

| CPI (y/y) | Actual | Prior |

Expected |

| Headline | +2.4% | +2.3% | +2.5% |

| Core | +2.8% | +2.8% | +2.9% |

Headline PPI rose in May, while Core PPI fell. April data was revised higher by +0.1%.

| PPI (y/y) | Actual | Prior |

Expected |

| Headline | +2.6% | +2.5% | +2.6% |

| Core | +3.0% | +3.2%* | +3.1% |

This week, May retail sales data comes out Tuesday, FOMC makes another interest rate decision Wednesday, and US markets are closed Thursday for Juneteenth.

Best to Your Week!

P.S. If you find this research helpful, please tell a friend.

If you don’t, tell an enemy.