Stock Market Outlook entering the Week of July 31st = Uptrend

-

- ADX Directional Indicators: Uptrend

- Price & Volume Action: Uptrend

- Elliott Wave Analysis: Mixed

ANALYSIS

The stock market outlook kicks off week 2 of an uptrend, as stocks went risk-on despite an interest rate hike, negative GDP print, and continued earnings deceleration.

The S&P500 ($SPX) found support at the 50-day moving average Tuesday, closing the week up 4.3%. The index is back near highs of early June, or lows of March, whichever you prefer. Either way, that zone creates a lot of overhead resistance (i.e. bag holders) for traders to work through.

SPX Price & Volume Chart for the Week of July 31 2022

No change in the underlying signals: ADX shows a bullish trend, as does the Price/Volume signal, while Elliott Wave is mixed.

SPX Elliott Wave Analysis for the Week of July 31 2022

The bearish count, shown above, puts the market towards the end of the ongoing bear market bounce, with the index closing just above a target range for the C-wave of a 3-3-5 “flat” pattern. The RSI didn’t confirm a top (via a divergence), but that’s not necessarily required to end a corrective flat (see late March). A plausible (but not yet probable) bullish count, with the entire correction ending at the mid-June low, puts the SPX in the middle of the first wave of the next bull market.

COMMENTARY

“Better than expected” was last week’s mantra when it came to financial markets.

For earnings, we touched on the issue of beating estimates verses year over year comparisons. As of Friday morning, 264 companies in the S&P500 had reported, with aggregate, year-over-year earnings falling -2%. Even positive headlines weren’t all they were cracked up to be.

Take Apple ($AAPL) for instance. The company beat Wall Street expectations for sales and profit. But the year over year numbers weren’t great. Revenue was up 2%, but earnings per share were down 8%. So even though their sales increased, their expenses increased more.

Amazon ($AMZN) also reported financial results, with a similar story to Apple. Headlines said the company reported better-than-expected Q2 revenue ($121B actual vs. $119B expected) and the outlook for Q3 was “upbeat”. What about earnings; you know, actual profit? That figure came in at a loss of 20 cents per share. The company also cut ~100k people from it’s workforce.

Some will point out that there are investment related losses in Amazon’s EPS figure, which is true. There’s ~$2B in losses from their investment in the electric truck manufacturer Rivian alone. So look at operating income, which excludes the investment-related losses. That metric hit $3.3 billion…down from $7.7 billion in Q2 of 2021…or 57% lower y-o-y.

The result? Amazon’s stock price rallied 13%. You’d be hard pressed to find an answer to “tell me we’re in a bear market bounce without telling me we’re in a bear market bounce”.

The U.S. Federal Reserve hiked short-term interest rates another 0.75%. Chairman Powell slipped in a reference to approaching the “natural interest rate” (whatever that means), and many people interpreted that as a sign the worst is over from a tightening perspective. Then I read an opinion that instead of 0.75% to 1% hikes, the Fed is only expected to hike 0.50, 0.25, and 0.25 over the next 3 meetings. We must have been watching different press conferences.

Inflation has likely peaked, as we discussed before. But even if it gets cut in half by the end of the year, which is unlikely, it would STILL be double the Fed target of 2%. And that doesn’t even consider the ongoing impact of the Fed balance sheet reductions.

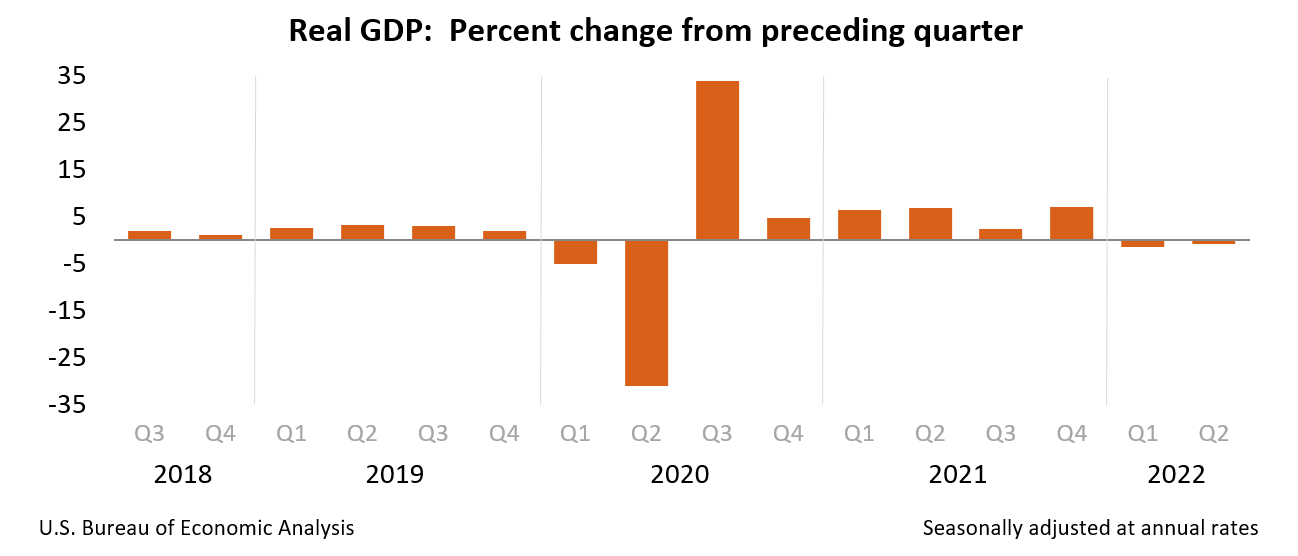

Q2 GDP couldn’t keep up with expectations though, contracting -0.9% (a small increase increase was expected). The reading is the second consecutive quarter of negative growth (Q1 declined 1.6%).

Source: Bureau of Economic Analysis

Since the common definition of a recession is two consecutive quarters of negative GDP, you can see why there was so much airtime devoted to the topic last week. It seems that the 2 quarter definition is actually a rule of thumb, not anything “official”. Pundits argue that the U.S. can’t be in a recession because:

- The consumer is “strong”

- Corporate earnings aren’t “as bad as expected”

- Unemployment is “low”

It’s all relative of course, which means being “selective with data” like consumer spending and earnings comparisons as we’ve reviewed in prior posts. But unemployment really is low verses historical data, so I guess 1 out of 3 isn’t bad. And we can always slice and dice employment data if the recession picks up speed and unemployment threatens to increase.

Financial media (social, online, and otherwise) is awash in calls that the bottom is in, and it’s time to get off the sidelines. Unfortunately, that’s not how market bottoms are made, from a sentiment perceptive.

Rest assured, the next bull market is coming, and will offer great buying opportunities. But those opportunities typically occur when retail investors throw in the towel and are disgusted with stocks, not buying them because data isn’t as bad as expected.

In the meantime, look for companies that provide products and services you need to buy regardless of inflation (e.g. consumer staples ($XLP) and utilities ($XLU) ), with low beta values.

Best To Your Week!

P.S. If you find this research helpful, please tell a friend. If you don’t, tell an enemy.