Stock Market Outlook entering the Week of July 17th= Downtrend

-

- ADX Directional Indicators: Downtrend

- Price & Volume Action: Mixed

- Elliott Wave Analysis: Mixed

ANALYSIS

The stock market outlook stays with the downtrend, since the S&P500 didn’t make much progress last week. The S&P500’s ($SPX) second attempt to break-through May resistance levels failed, and now we’re on to the third. For the week, the index fell 0.9%.

SPX Price & Volume Chart for the Week of July 17 2022

No change in the ADX directional indicators (bearish) or price/volume action (mixed). And add two more distribution days.

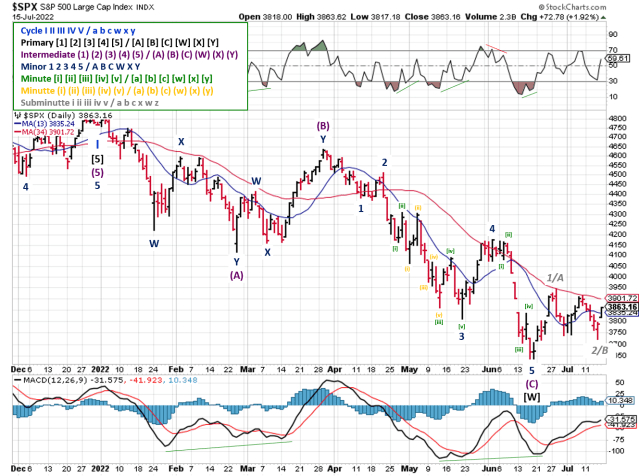

SPX Elliott Wave Analysis for the Week of July 17 2022

The Elliott Wave signal retreats to mixed this week. The S&P500 briefly fell below last week’s “higher low”, breaking support at 3739. As mentioned last week, trading firms actively trade support and resistance levels, so the recover Thursday and Friday isn’t that surprising.

COMMENTARY

US CPI data for June showed an increase of 9.1% verses a year ago and 0.5% higher than last month. Expectations were already high (8.8%), so coming in below expectations wouldn’t REALLY be something to celebrate. The smallest sliver of a silver lining was Core CPI, which +5.9% higher than last year, but down from the 6% y-o-y reading last month.

This situation is playing out across the globe, not just the United States. Take a look at some CPI data from Europe:

- Denmark = up +8.2% from +7.4%

- France = up +5.8% from +5.2%

- Germany = flat at +7.6%

- Norway = up +6.3% from +5.7%

- Portugal = up +8.7% from +8.0%

Another key inflation dataset, the U.S. producer price index (PPI), reported an increase of 11.3% y-o-y. Finally, the spread between 2-year and 10-year treasury notes hit -26 basis points (biggest negative spread in 22 years), ended the debate about yield curve inversion.

Even if future rate hikes are already priced in (June CPI & PPI guarantee more hikes) and the effect of quantitative tightening negated (it isn’t), most corporate earnings guidance hasn’t been taken down yet. The few firms that have made adjustments (e.g. Target, Walmart, Restoration Hardware) saw their stock price crushed.

What happens to the market if/when companies with large weightings (e.g. Apple, Google, Tesla) decide to revise guidance lower? We’ll soon find out. Earnings season kicked off last week, with JP Morgan missing estimates and suspending its stock buyback program, citing “‘never-before-seen” conditions. Morgan Stanley didn’t fair much better. Both stocks were hammered. Citigroup beat expectations and maintained guidance for the year, and enjoyed some pretty strong price action.

DO NOT base investment decisions on the fact that a stock is down double-digit percentages from an all time high. When someone says a stock is “cheap” because its price has been cut in half, they’re assuming the stock was valued correctly in the first place. Chances are it was not, and that’s before considering the new interest rate environment going forward.

Rising interest rates increase the cost of capital, which increases corporate expenses and suppresses future earnings growth. So as long as central banks are changing interest rates and financial conditions, valuations and stock prices also need to be adjusted.

In other words, a stock that looks “cheap” verses a year ago (low interest rates, economy re-opening, stimulus checks and quantitative easing) may actually still be “expensive” when compared to future earnings (rising interest rates, recession, quantitative tightening).

Best To Your Week!

P.S. If you find this research helpful, please tell a friend. If you don’t, tell an enemy.